Reigniting Women-led Businesses in the Caribbean with Better Access to Finance

New data from the Caribbean shows that high collateral requirements and interest rates are among the top barriers for women-owned and -led businesses looking for financing. Overcoming these hurdles is an important challenge for the Caribbean, especially as firms seek to regain a foothold in a post-pandemic private sector.

It is no secret that despite their importance, micro, small, and medium enterprises (MSMEs) – accounting for 99.5% of firms in Latin America and the Caribbean, or LAC – face big hurdles in accessing the financing they need to innovate, invest, and grow. This problem is even more pronounced for MSMEs owned or led by women.

In the Caribbean region, women-owned/led firms tend to be on the smaller end of the MSME spectrum, with fewer employees on average. Moreover, recent evidence from the Caribbean suggests that women-owned/led firms were more negatively impacted by the COVID-19 pandemic relative to other firms.

Against this backdrop, what do Caribbean women entrepreneurs themselves have to say about what’s holding them back from accessing finance? A new report by the IDB’s Caribbean Department, IDB Invest, and Compete Caribbean analyzes self-perceived barriers to financial access using firm-level data for over 1,000 firms in 6 Caribbean countries, drawing on the Compete Caribbean enterprise surveys. Analyzing the data, we have identified the most persistent barriers faced by women-owned/led businesses versus their male-led peers. Additionally, we draw on examples of how the IDB Group is working to improve financial access for women-led MSMEs.

What are some of the main takeaways?

- Women-owned/led business are more likely to rely on short-term financing. Our data indicates that over the last 20 years, women-owned/led firms accessed approximately 20% of the volume of all short-term credit granted in each country (loans with a maturity less than three years). These include lines of credit, overdraft facilities, and credit cards. Importantly, they only accessed 1.3% of medium-to-long term loans over the same period. These short-term instruments also tend to have higher borrowing costs.

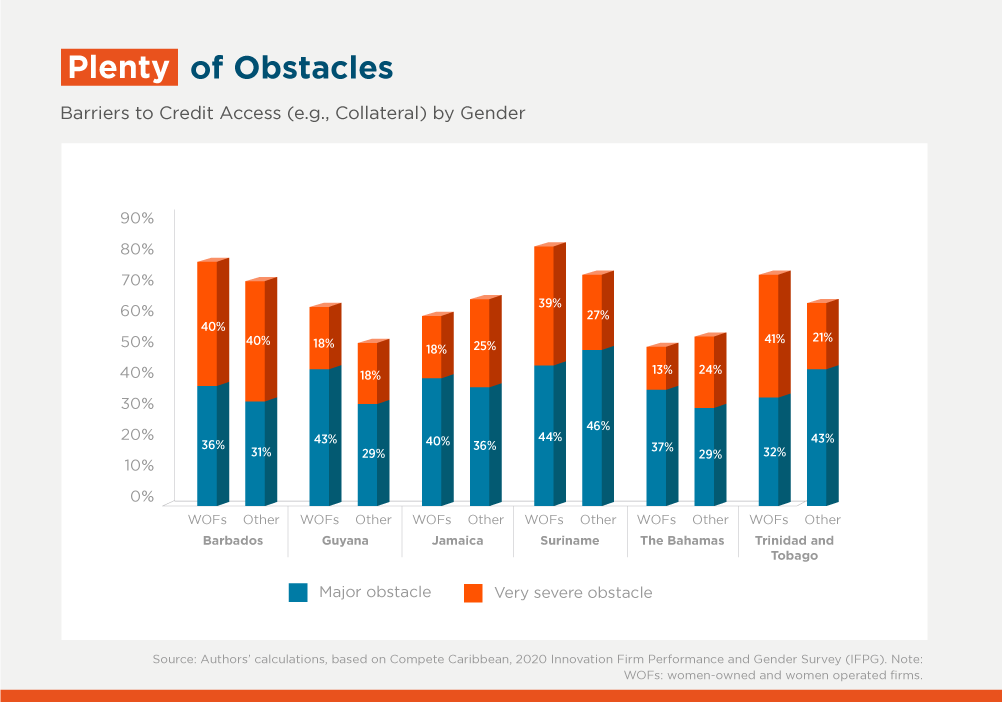

- Two-thirds of women-owned/led firms report access to finance as a major or severe obstacle to business. In most Caribbean countries, a higher proportion of women-owned/led firms cite barriers to accessing credit, particularly collateral requirements as a major or severe obstacle relative to other firms. This difference is most noticeable in Guyana and Suriname, where women-owned/led firms are 14 and 10 percentage points more likely, respectively, to have this view.

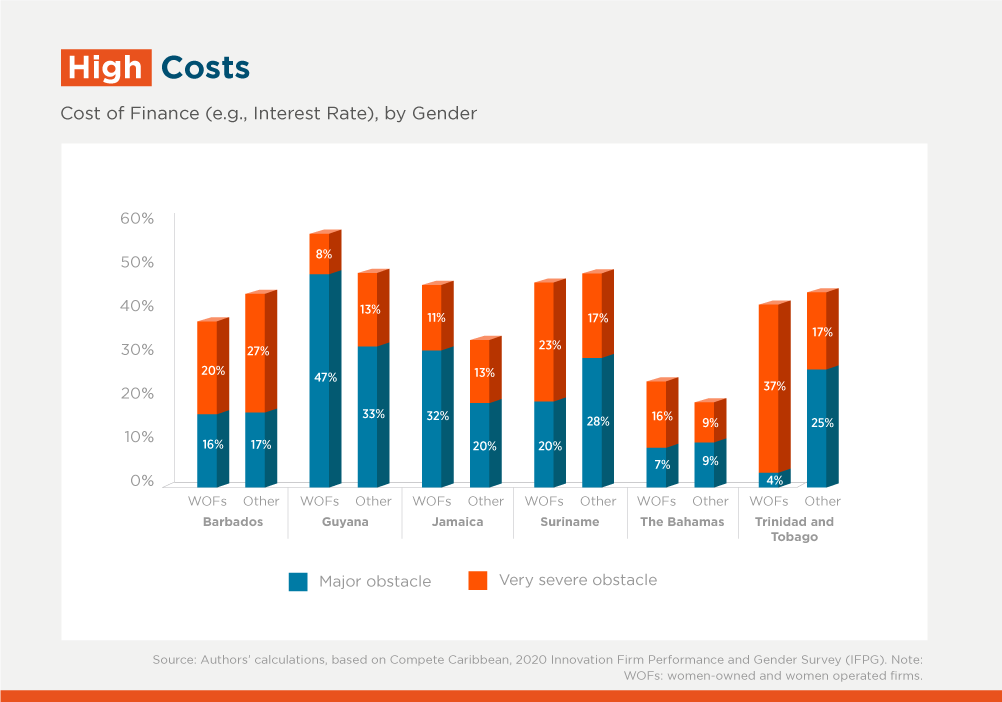

- The cost of finance also plays a role in overall financial development. 39% of women-owned/led firms view high interest rates as a major or severe obstacle to doing business. In Guyana, Jamaica, and The Bahamas a higher proportion of women cite cost of finance as a major or severe obstacle relative to other firms. Interestingly, in Barbados and Suriname where more women-owned/led firms cite access to finance as a major obstacle relative to other firms, the cost of finance isn’t the main reason. For example, 76% of women-owned/led firms in Barbados cite access to finance as a barrier, but only 36% say that the cost of finance is a hurdle. This suggests that other factors are at play, such as the terms of loans (tenor) and how they are structured, the ability to secure enough collateral, or a lack of capacity to successfully apply for and obtain business loans. Notwithstanding, overall, 31% of women-owned/led firms in the region that decided not to apply for a loan reported unfavorable interest rates as the reason (the highest single reason cited).

- Financial institutions can do more to boost the growth of women-owned/led firms. Multilateral and development finance institutions are working hand-in-hand with the financial sector to develop solutions to increase access to finance for women-owned/led firms. For example, the Women Entrepreneurs Finance Initiative (We-Fi) is an international alliance that aims to unlock financing and access to markets for companies owned or led by women. With financing from We-Fi, IDB Invest provided performance-based incentives and advisory services to help Banco Promerica in the Dominican Republic grow its portfolio of women-led SMEs. Initiatives like this can provide a model for future interventions seeking to expand access to credit for women.

By gaining access to finance, women-owned/led firms can overcome constraints that would otherwise prevent them from growing. We should continue to learn from interventions that have helped private financial institutions increase their financing of women-led SMEs, as they can serve as a blueprint for promoting more and better access to finance for women across the region.

For more details, see the July 2022 edition of the Caribbean Economics Quarterly, Finance for Firms: Options for Improving Access and Inclusion.

(Khamal Clayton and Monique Graham of the IDB’s Caribbean Country Department are also contributors of this report.)

Authors

María Cecilia Acevedo

Maria Cecilia Acevedo is a Lead Strategy Officer in the Strategy and Development Effectiveness Department at IDB Invest in Washington, DC. María Cecilia leads the preparation of country strategies for IDB Invest, in particular providing technical analysis by including the private sector perspective for Latin America and the Caribbean. María Cecilia conducts research on economic development issues, especially on the contribution of the private sector to the welfare of the population and the mechanisms through which market solutions are efficient to achieve this objective. A Colombian national, María Cecilia received her M.A. and Ph.D. from Harvard University, and an M.A. in Economics from Universidad de los Andes, Bogotá.

Natasha Richardson

Natasha Richardson is the IDBG Regional Private Sector Coordinator for the Caribbean Region. Natasha has worked in private sector development for the past 23 years in a variety of roles both with development finance institutions and directly with a private sector company. A dual citizen of Jamaica and Canada, Natasha holds a Master of Business Administration from the Ivey Business School – Western University and an H.B.A. from the University of Toronto with a specialization in International Relations and a minor in Spanish.

Stefano Pereira

Stefano Pereira is Senior Development Impact Advisor at FinDev Canada where he is a contributor the organization’s thought leadership agenda. Prior to joining FinDev Canada, he worked in the Development Effectiveness Division at IDB Invest. His areas of research include private sector development, productivity and green economics and his work has been featured in books, technical papers and academic journals. He holds an M.A. in Economics from the University of Toronto and B.A. in Economics from the University of the West Indies.

David Rosenblatt

David Rosenblatt is the Regional Economic Adviser for the Caribbean Country Department at the Inter-American Development Bank (IDB). Prior to this position, David worked for 27 years at the World Bank, where he divided his career between assignments in the Latin America and Caribbean region and the World Bank Chief Economist’s office. David holds a Ph.D. in Economics from the University of California, Berkeley.

Henry Mooney

Henry Mooney serves as Economics Advisor with The Inter-American Development Bank. He previously worked with investment bank Morgan Stanley in London, The International Monetary Fund (IMF), World Bank, and Government of Canada, including on dozens of advanced and emerging market economies in Africa, Asia, Europe, Central Asia, Latin America and the Caribbean. Henry's responsibilities have included leading regional macroeconomic and financial research publications, serving as chief and team leader for IMF and World Bank technical assistance and financing operations focused on sovereign debt issuance, debt restructuring, and public financial management, as well as producing economic forecasts in the context of adjustment programs and surveillance. Henry is a dual Brazilian and Canadian citizen, who completed his studies in economics and finance at Concordia University (BA), The London School of Economics (MSc), The University of London (PhD), and Harvard University (MPA).

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

SubscribeGender

Related Posts

Digital Innovation Expands Financing for Women-Led SMEs in Latin America and the Caribbean

Loans and disbursements approved in less than 24 hours, enabled by artificial intelligence, and early invoice payments powered by fintech solutions are transforming access to credit for MSMEs, especially those led by women.

Fixing the Broken Rung: How Data Can Help Advance Women’s Careers in Latin America and the Caribbean

In Latin America and the Caribbean (LAC), the greatest disruption in women’s career progression occurs during the transition into managerial roles. A collaboration between IDB Invest and LinkedIn, within the framework of the Development Data Partnership, uses large-scale labor-market data to identify where women’s participation declines and what barriers exist across sectors and career stages.

Addressing gender-based violence from the private sector: the experience of Laboratorios Bagó

Francisco Méndez, CEO of the pharmaceutical company, shares his company's efforts and achievements in fostering an inclusive and safe work environment.