Eliminating Gender Bias from Lending in Mexico

The Mexican fintech Konfío is eliminating gender bias by using fair algorithms to make lending decisions based only on applicants’ credit risk. A new IDB Invest study that measures the impact of a Konfío loan on company sales shows that women-led businesses have the most to gain.

A common belief is that women are more risk-averse than men. Paradoxically, many financial institutions see women as higher-risk clients, leading to less favorable credit offers compared to their male counterparts—smaller amounts, shorter tenors, and higher rates and collateral requirements. This means that women-led businesses face greater barriers to accessing the credit they need to manage and grow their business.

This is a loss for both women and the economy, as women-led businesses also tend to hire more women than male-led companies. Additionally, banks miss out on millions of dollars in profits, as we have confirmed with various financial institutions in the region. Part of the problem lies in the entrenched gender biases that affect lending decisions and the terms offered.

How can we unroot these deep gender biases in the financial sector? Fintechs may have an answer.

Fintechs have revolutionized the world of finance, enabling greater access to financial products and services. They have a big impact on inclusion, as they have huge potential to ensure equal, unbiased access to credit. Many fintechs rely on automated, sophisticated algorithms and mathematical models to make their lending decisions.

While algorithm fairness is not a given, a well-designed one with minimal human involvement in the decision-making process can eliminate the biases—related to gender, ethnicity or origin—that negatively affect the financing options offered.

This is the case of the Mexican fintech Konfío. As part of our work with the company, we audited their algorithm and concluded that there’s an identical credit offer for both men and women. In addition, we compared repayment behavior of the two groups and confirmed that it is identical. However, an equal credit offer for both men and women is the exception rather than the rule among financial institutions in Mexico and the rest of the region.

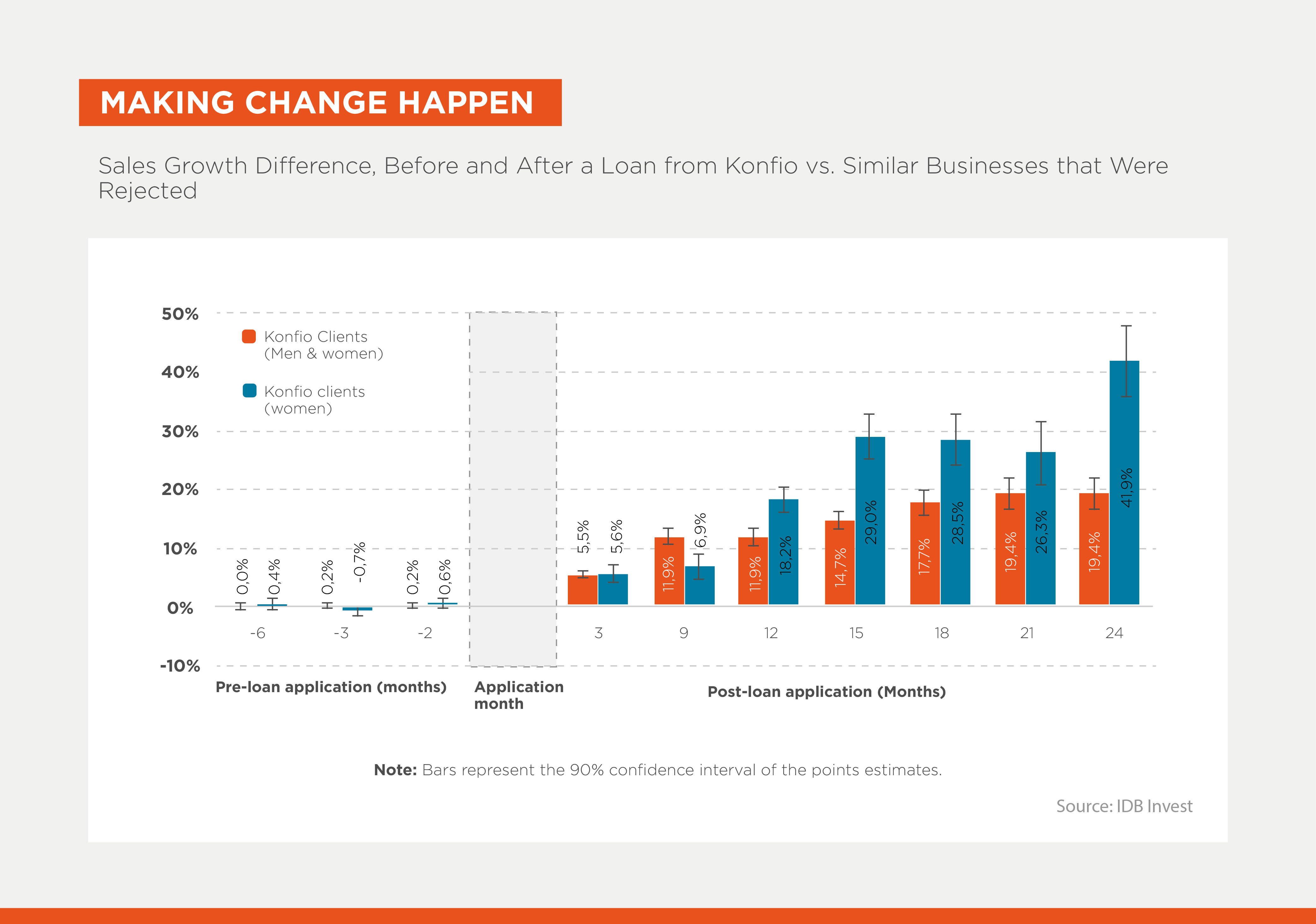

We’ve also worked with Konfío to estimate the impact of their lending on companies’ sales growth. We found that two years after receiving a loan from Konfío, companies’ sales growth was 19% higher than that of similar businesses whose application had been rejected. Among Konfío’s female clients, sales grew by more than 42% compared to similar women-owned businesses whose application had been rejected.

The question then is: Why is the growth rate more than twice as high when we only consider women-owned businesses?

Since it is often harder for women-owned businesses to access credit and, when they do, it is typically on less favorable terms, it is likely that the women-owned businesses rejected by Konfío experienced lower growth rates than the rejected male-owned companies, which likely had easier access credit elsewhere. In short, the large difference in sales growth among women is likely less due to Konfio’s female clients performing better, and more due to the other women performing much worse due to prevailing credit market constraints in Mexico.

This situation offers a unique opportunity for fintechs in Mexico and the region. If these financial service providers define a gender strategy from the outset and mitigate potential biases in their lending process, they will grow by attracting an underserved segment that is ready to make the most of these loans.

These gender-inclusive fintechs will have a unique advantage over their competitors, as women tend to be loyal customers. The provider that serves the women’s segment first is more likely to keep them in their portfolio.

If all financial institutions in Mexico and the region were able to remove gender bias from their loan offers, women-owned businesses could achieve their full growth potential, while driving the region’s economic growth without damaging financial institutions’ performance. It would be a win-win. There is nothing risky about that.

For more information about the study discussed in this blog, check out the DEBrief by Irani Arráiz (2023) “Boosting Business Growth while Leveling the Credit Playing Field for Women MSMEs in Mexico”.

Authors

Irani Arraiz

Irani Arráiz es economista en la División de Efectividad en el Desarrollo de BID Invest. Sus áreas de experticia incluyen evaluación de políticas y finanzas y desarrollo del sector privado. Ha publicado varios artículos en revistas académicas internacionales relacionados con la efectividad de programas destinados a aumentar la competitividad del sector privado en América Latina. Antes de BID Invest, Irani trabajó en el Fondo Multilateral de Inversiones y en la Oficina de Evaluación y Supervisión del BID. Irani tiene un Ph.D. en Economía de la Universidad de Maryland en College Park, la designación de CFA, y un MBA del Instituto de Estudios Superiores de Administración en Venezuela. Irani se graduó con honores como ingeniero electrónico en la Universidad Simón Bolívar en Caracas.

Carlos Roberto Argüello

Isabel Berdeja

Isabel is a Gender, Diversity and Inclusion Officer at IDB Invest, where she joined in 2019. Isabel is responsible for designing and executing advisory services for deals in the financial and corporate institutions sectors. She has led advisory engagements to support clients in their diversity and gender inclusion strategies, with an emphasis on the inclusion of indigenous and Afro-descendant peoples throughout the value chain and in the workforce. Before joining the IDB Group, Isabel worked for General Electric in the energy business and at the Pan American Development Foundation in the execution of projects for the development with identity of indigenous peoples. Isabel earned a master's degree in development studies from the Elliott School at George Washington University in Washington, D.C. She also has a bachelor's degree from the Universidad Iberoamericana Mexico.

LIKE WHAT YOU JUST READ?

Subscribe to our mailing list to stay informed on the latest IDB Invest news, blog posts, upcoming events, and to learn more about specific areas of interest.

Subscribe{{ raw_arguments.field_category_target_id }}

Related Posts

Korea's Cutting-Edge Innovations to Transform Agribusiness in Latin America and the Caribbean

Discover how IDB Invest connects regional agribusinesses with leading innovators in Korea to accelerate smart agriculture, agritech, and sustainable growth.

Digital Transformation Redefines Agricultural Competitiveness in Latin America and the Caribbean

Every time an agricultural company determines when to irrigate, selects what inputs to apply, or decides how to market or transport its production, the use of data and technological solutions becomes a key competitive advantage.

Combating Multidimensional Poverty from the Private Sector Requires Much More Than Jobs

For Danper, a leading Peruvian company in the global agri-food sector, understanding the living conditions of its workers and their families is fundamental to strengthening actions to improve their quality of life.